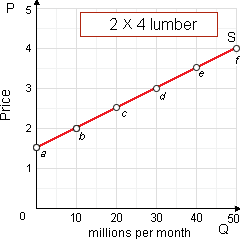

The section of this supply curve for 2×4s which is least price elastic is in between: (i) point a and point b. (ii) point b and point c. (iii) point c and point d. (iv) point d and point e. (v) point e and point f.

Hey friends please give your opinion for the problem of Economics that is given above.