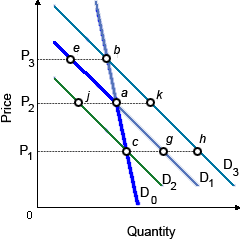

Within this kinked demand curve model, when this firm operated at point a and increased its price from P2 to P3 but other firms did not increase their prices, in that cases equilibrium for this firm would move to be: (w) point b. (x) point e. (y) point g. (z) point k.

Can someone explain/help me with best solution about problem of Economics...