Determine competitive price of purely competitive firm

In this demonstrated figure purely competitive lumber mill’s generic 2×4s now sell for: (1) $3.60 each. (2) $3.00 each. (3) $2.70 each. (4) $2.40 each. (5) $2.10 each. Can someone explain/help me with best solution about problem of Economics...

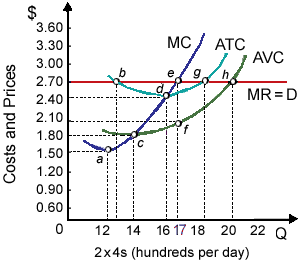

In this demonstrated figure purely competitive lumber mill’s generic 2×4s now sell for: (1) $3.60 each. (2) $3.00 each. (3) $2.70 each. (4) $2.40 each. (5) $2.10 each.

Can someone explain/help me with best solution about problem of Economics...

Whenever stockholders who made big financial investments in Enron prior to the mid-1990s suffered huge losses during the year 2001-2002 since of deceptive accounting practices and insider trading, they were the victims of problem termed as: (1) Adverse selection (2) M

A demand curve has a slope which would be expressed as like $5/ (1 extra ton demanded) when a: (w) 5 % price cut raises quantity demanded by 1 %. (x) $5 price cut increases quantity demanded by 2000 lbs. (y) $5 price hike boosts quantity supplied by 2

The price elasticity of supply in given grph is infinite therefore supply is perfectly price elastic within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Q : Lowest price in shopping for expected Consumers shop for the lowest price probable for a good only till the expected benefits of shopping no longer go beyond the expected: (w) maximum legal prices for the good. (x) prices available in the black market. (y) transaction costs related with a

Consumers shop for the lowest price probable for a good only till the expected benefits of shopping no longer go beyond the expected: (w) maximum legal prices for the good. (x) prices available in the black market. (y) transaction costs related with a

Types of measurement in Metrics: A) Nominal: a nominal scale assigns items to a category. For example, the category may be a simple "yes" or "no." In the case of a family, a nominal scale

The price makers in a purely competitive market are: (i) pure competitors or perfect competitors. (ii) producers of capital goods. (iii) pure oligopolies. (iv) monopolistic competitors. (v) pure monopolies. H

Select the right answer of the question. A competitive market will: A) achieve an equilibrium price. B) produce shortages. C) produce surpluses. D) create disorder.

Nostalgia Corporation has controlled to lock-up the rights to each black-and-white film ever made, as well as the response to its infomercials has been astounding. The initial point Nostalgia requirement to identify in its quest to maximize profit is:

LoCalLoCarbo has become the favorite of fad dieters. There in curve E shows: (1) LoCalLoCarbo’s marginal cost curve. (2) LoCalLoCarbo’s average variable cost curve. (3) LoCalLoCarbo’s average total cost curve. (4) the market demand curve facing LoCal

I have a problem in economics on Analytic Time-The Short Run. Please help me in the following question. In short run: (1) At least one resource is fixed. (2) Firms can enter or exit the industry. (3) Economies of the scale are present. (4) Total fixed cost rises with

18,76,764

1943628 Asked

3,689

Active Tutors

1435853

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!