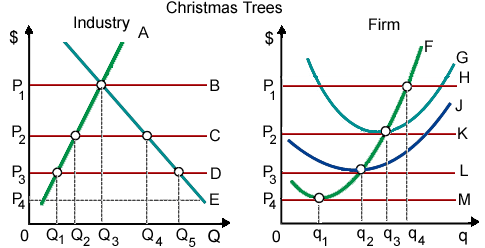

As din demonstrated curve J in below is this Christmas tree: (w) industry’s supply curve. (x) firm’s demand curve. (y) firm’s average variable cost curve. (z) firm’s short-run supply curve.

Hey friends please give your opinion for the problem of Economics that is given above.