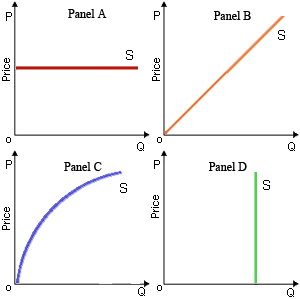

The quantity supplied is ever more sensitive as output increases, therefore the price elasticity of supply raises as the price raises for the supply curve demonstrated in: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?