Demand perfectly price elastic immeasurable

Demand is perfectly price elastic when the price for Pixie's cheesy fried grits is a mostly unmeasurably small bit below the: (1) zero. (2) P1. (3) P2. (4) P3. (5) P4. Please choose the right answer from above...I want your suggestion for the same.

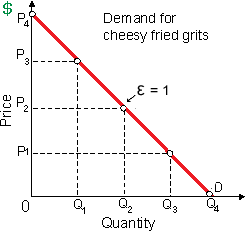

Demand is perfectly price elastic when the price for Pixie's cheesy fried grits is a mostly unmeasurably small bit below the: (1) zero. (2) P1. (3) P2. (4) P3. (5) P4.

Please choose the right answer from above...I want your suggestion for the same.

How is a shift in demand reflected in a demand equation? How is a shift in supply reflected in a supply equation? How is a movement along a demand (supply) curve reflected in a demand (supply) equation?

During product differentiation, the firms attempt to: (w) become price takers. (x) gain a degree of market power over their pricing and sales of their products. (y) increase the supply of their products. (z) raise the price elasticity of the demand fo

The price a firm acquires from selling an extra unit of output, minus any revenue lost when price should be reduced in all other units sold, equals: (1) average revenue. (2) marginal profit. (3) mark-up price. (4) marginal revenue. (5) total revenue.<

Payments for a resource into excess of the minimum needed to supply specified amounts of the resource are termed as: (1) economic rents. (2) wage premiums. (3) excess profits. (4) surplus values. (5) capitalization. Q : Short-run supply curve for a For a competitive firm, the short-run supply curve is the portion of its: (w) AVC curve that lies above the ATC curve. (x) MC curve which rises above its AVC curve. (y) MC curve which is upward sloping. (z) AFC curve which lies above the MC curve.

For a competitive firm, the short-run supply curve is the portion of its: (w) AVC curve that lies above the ATC curve. (x) MC curve which rises above its AVC curve. (y) MC curve which is upward sloping. (z) AFC curve which lies above the MC curve.

When price falls and quantity rises along a negatively-sloped linear demand curve: (1) total revenues fall till elasticity equals zero, then this rises. (2) demand is decreasingly price elastic. (3) there is a contrad

Choose the right answer from following. Tariffs: A) may be imposed either to raise revenue (revenue tariffs) or to shield domestic producers from foreign competition (protective tariffs). B) are also called import quotas. C) are excise taxes on goods exported abroad.

When curve C reflects the long run supply curve as in demonstrated figure for this industry, in that case this is a/an: (w) decreasing cost industry. (x) increasing cost industry. (y) constant cost industry. (z) diseconomies of scale industry.

Assume that a monopolist face a stable negatively-sloped demand curve. Making more sales needs the monopolist to: (1) advertise its product. (2) decrease the price of the product. (3) lower its marginal revenue. (4) improve its technology. (5) increas

When the preference for current consumption over future consumption strengthens, in that case the: (w) interest rate rises. (x) interest rate falls. (y) present value of future income rises. (z) interest rate remains the same. How

18,76,764

1942934 Asked

3,689

Active Tutors

1459477

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!