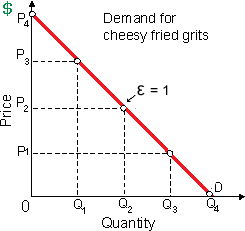

From these points in this figure, demand for cheesy fried grits is largely elastic at a price of: (w) P1 and quantity of Q3. (x) P2 and quantity of Q2. (y) P3 and quantity of Q1. (z) P4 and quantity of 0.

Can someone explain/help me with best solution about problem of Economics...