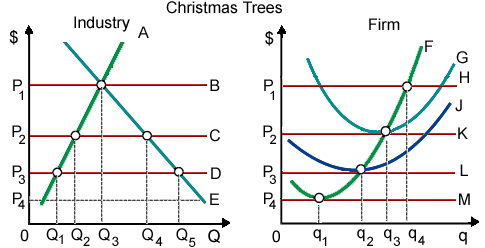

For Christmas tree in this market, Curve H is this: (w) industry’s long-run supply curve. (x) firm’s demand curve in the short run. (y) industry’s marginal cost curve. (z) firm’s long run marginal cost curve.

Can someone explain/help me with best solution about problem of Economics...