Define regressive in taxes as percentage of income

Line T2 depicts as in below graph a tax system which is: (i) progressive. (ii) recessive. (iii) proportional. (iv) biased. (v) regressive. How can I solve my economics problem? Please suggest me the correct answer.

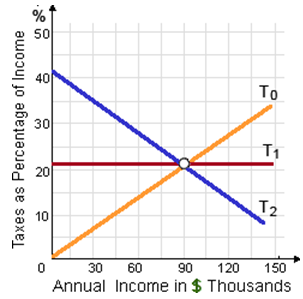

Line T2 depicts as in below graph a tax system which is: (i) progressive. (ii) recessive. (iii) proportional. (iv) biased. (v) regressive.

How can I solve my economics problem? Please suggest me the correct answer.

You are more probable to shop at a remote farmers’ market quite than buy apples at a local grocery store while: (w) possible, since produce is cheaper at the farmers’ market. (x) you would like to buy only vegetables and fruits. (y) the opportunity costs o

Select the right answer of the question. U.S. export transactions create: A) a U.S. demand for foreign monies and the satisfaction of this demand decreases the supplies of dollars held by foreign banks. B) a U.S. demand for foreign monies and the satisfaction of this

Predictions which higher gasoline prices will increase total spending on gas imply such as the demand over the relevant price range that is: (w) unlimited. (x) relatively price elastic. (y) unitarily price elastic. (z) relatively price inelastic.

Long-run supply curve of a purely competitive industry: (w) equals the horizontal summation of all firms’ short-run supply curves. (x) reflects equilibrium outputs after entry and exit respond completely to any shifts in demand. (y) declines as

A monopoly is a type of market structure in that one: (w) seller makes up the industry. (x) giant firm is a price taker. (y) barrier to entry exists. (z) giant firm is the particular buyer of resources. Q : Public Goods and Service Why does a Why does a good or service become a public good or service?

Why does a good or service become a public good or service?

When a monopolist maximizes the profit in a product market, it will: (w) Hire labor till the marginal revenue product equivalents marginal resource cost. (x) Hire labor till the value of marginal product equivalents marginal resource cost. (y) Pay a wage equivalent to

The price elasticity of demand would possibly be lowest for: (1) Dasani. (2) Deer Park. (3) Aquafina. (4) bottled water. (5) Perrier. Can anybody suggest me the proper explanation for given problem regarding

Outputs and average prices for CDs and DVDs both rose throughout 1999 to 2000 (just before file sharing became ordinary), implying such that: (1) supply of prerecorded music should have grown. (2) law of demand does not apply to music. (3) demand for

The economy consists of an equal number of smokers (S-types) and asthma sufferers (A-types). Good 1 is cigarettes, good 2 is “other stuff.” S-types have the utility function: xS1 + xS

18,76,764

1957539 Asked

3,689

Active Tutors

1422546

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!