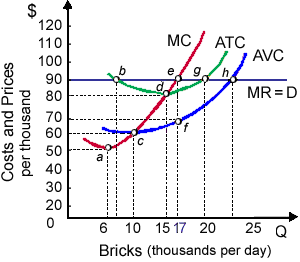

Decreased market demand for generic bricks would result in a(n) ___________ in the price of bricks and a(n) ___________ in this brickyard’s profit-maximizing output. (w) increase; decrease. (x) increase; increase. (y) decrease; decrease. (z) decrease; increase.

Hey friends please give your opinion for the problem of Economics that is given above.