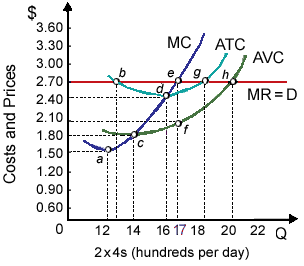

Decreased market demand for generic 2×4s as in illustrated graph would result within a(n) ___________ into the price of 2×4s as well as a(n) ___________ in this lumber mill’s profit-maximizing output. (w) increase; decrease. (x) increase; increase. (y) decrease; decrease. (z) decrease; increase.

Please choose the right answer from above...I want your suggestion for the same.