Consumption curve

Illustrate a point on consumption curve at which APC = 1. Answer: APC = C/Y = 1 is possible when C = Y, that is, Consumption is equivalent to Income.

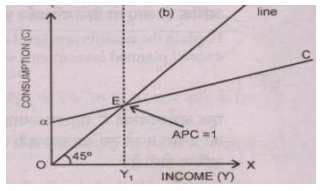

Illustrate a point on consumption curve at which APC = 1.

Answer:

APC = C/Y = 1 is possible when C = Y, that is, Consumption is equivalent to Income.

‘Must a country which is less proficient at generating all goods use import controls to decrease imports from additional countries?’

A flat rate income tax for all levels of income along with no exceptions would be taken as a: (i) proportional tax. (ii) progressive tax. (iii) regressive tax. (iv) common tax. Can anybody suggest me the proper exp

Please brief the knowledge what is long run supply?

discuss with the help of IS-LM model why money has no effect on output in classical supply case

When this market starts in equilibrium at point e on S0D0 and then young American families rousingly “inherit” furniture as their baby-boomer parents shift into smaller retirement homes, then this market will tend to shift in the direction of: (i) point i.

When a tax on goat cheese is completely paid by consumers via higher prices, then the tax has been: (i) alleviated. (ii) Forward shifted. (iii) Backward shifted. (iv) Actualized. (v) Randomized. Can someone help me in getting throu

Harsher punishments for drug dealers than for addicts can’t be blamed for higher: (1) rates of police corruption because main dealers can present big bribes. (2) rates of street crime by addicts. (3) profits reaped by successful pushers who are uncaught. (4) rat

As longer time periods are taken and a bigger range of adjustments (or substitutions) become obtainable, then demand curves tend to become: (1) flatter, as supply curves become steeper. (2) Steeper as supply curves become flatter. (3) Flatter, and therefore do supply

With the help of graph discuss the determinants of transaction demand.

How Bank rates control the credit? Answer: Bank rate is the rate of interest at which the Central bank lends to Commercial banks. By increasing the bank rate centra

18,76,764

1949298 Asked

3,689

Active Tutors

1456332

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!