Constant price elasticity plausible for demand curve

Constant price elasticity equivalent to one for socket sets would be mainly plausible for demand curve as: (1) D1D1. (2) D2D2. (3) D3D3. (4) D4D4. (5) D5D5. Hello guys I want your advice. Please recommend some views for above economics problems.

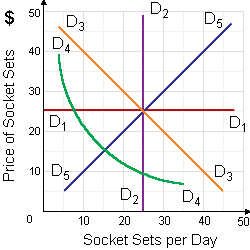

Constant price elasticity equivalent to one for socket sets would be mainly plausible for demand curve as: (1) D1D1. (2) D2D2. (3) D3D3. (4) D4D4. (5) D5D5.

Hello guys I want your advice. Please recommend some views for above economics problems.

This below figure demonstrates how consumption of goods A, B, C and D changes as a family’s income changes. When income increases, the income elasticity of demand is positive although declining for: (w) good A. (x) good B

Time Estimates for Individual Activities: A) Weighted Average Activity Time, t = (a + 4m + b)/6B) Standard deviation of activity times, σt = (b-a)/6C) Standard d

When a monopolist produces output where demand is unitarily elastic, in that case marginal revenue equals: (1) price. (2) infinity. (3) negative infinity. (4) one. (5) zero. I need a good answer on the topic of

Transfers to the poor “in-kind” are probably to be favored over cash transfer payments through: (a) people who are skeptical that the poor can manage their income competently. (b) economists concerned with improving effici

Economists suppose that nearly all decisions are made by: (i) At the margin. (ii) On the average. (iii) Based on totals. (iv) All of the above. Please someone suggest me the right answer.

When the equilibrium price of wheat is $50 per ton and the marginal cost of the last ton of wheat generated is $70, there is: (w) an efficiency loss to society from over-production. (x) an efficiency loss to society from underproducti

What does “buying on margin” means?

When numerous new firms enter a monopolistically-competitive market, in that case the demand curves facing the firms previously in that market will: (1) shift to the left and turn into more price elastic. (2) become straighter and less income elastic.

The LEAST compatible of such with the other three sets would be as: (w) entrepreneurship and innovation. (x) uncertainty and risk. (y) pure profit and monopoly. (z) patents and freedom of entry and exit. Hey friends please give you

In equilibrium for the firm with power to adjust the salary it pays, then the rate of monopsonistic exploitation equivalents any difference among: (i) VMP and MFC. (ii) MRP and MFC. (iii) P and MC. (iv) MRP and w. (v) MR and w. Fin

18,76,764

1937738 Asked

3,689

Active Tutors

1446061

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!