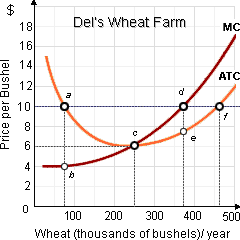

When Del’s production function and costs are characteristic for wheat farmers and when wheat farming is a constant cost industry, in that case in the long run, there the price of wheat will be: (i) $4 per bushel. (ii) $6 per bushel. (iii) $8 per bushel. (iv) $10 per bushel. (v) $12 per bushel.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?