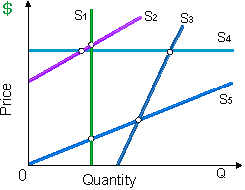

Comparing supply curves S2 and S3, supply is: (w) more price elastic along S2 than along S3. (x) more price elastic along S3 than S2. (y) equally elastic along both when they have similar slope. (z) unitarily elastic beside S3, and perfectly elastic along S2.

Hello guys I want your advice. Please recommend some views for above Economics problems.