Ceiling price problem

When the government obliged a ceiling price of P0 on papayas, the market scarcity would correspond to line: (1) ab. (2) cd. (3) ac. (4) bd. (5) ae. Can someone help me in getting through this problem.

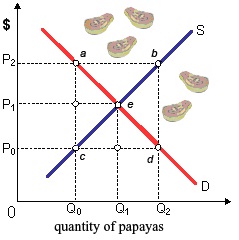

When the government obliged a ceiling price of P0 on papayas, the market scarcity would correspond to line: (1) ab. (2) cd. (3) ac. (4) bd. (5) ae.

Can someone help me in getting through this problem.

The advantages that firms confer on society do not comprise: (i) Decreasing the transaction costs. (ii) Raising consumer purchasing power. (iii) Facilitating the specialization in production. (iv) Raising the consumer demand. (v) Boosting the national income.

Total variable cost when this firm maximizes economic profits would be: (i) $12,000 per period. (ii) $24,000 per period. (iii) $32,000 per period. (iv) $48,000 per period. (v) $60,000 per period.

An increase in the supply of bonds tends to: (1) reduce the interest rate. (2) occur simultaneously with an increase in the demand for loanable funds. (3) yield an increase gross investment but a decrease in net investment. (4) drive up the prices of

When cost structures and the market demands facing each of the given types of firms were identical, in that case the greatest profits would be generated through a: (1) pure monopolist. (2) price discriminating monopolist. (3) perfectly competitive fir

Refer to the following diagrams, in which AD1 and AS1 are the "before" curves and AD2 and AS2 are the "after" curves. Other things equal, a decrease in resource prices is depicted by:1) panel (A) only. 2) panel (B) only. 3)

I have a problem in economics on Monopsony Power and Immobility of Labor. Please help me in the given question. The immobility of labor is economically significant as: (w) Most of the people like to move, however can't. (x) People in high salary occupations won't be c

This figure demonstrates a: (w) long run equilibrium for a firm in a perfectly competitive industry. (x) short run equilibrium for a natural monopoly. (y) short run circumstances for a monopolistically-competitive firm into long run equilibrium. (z) cartel which maxim

State economic arguments on whether a football club must sell a significant player?

This purely-competitive producer’s generic bricks presently sell for: (i) $60 per thousand. (ii) $70 per thousand. (iii) $80 per thousand. (iv) $90 per thousand. (v) $100 per thousand. Q : Transaction Costs-Process of trial and In an uncertain globe, people are supposed to try to make best use of their satisfaction by: (1) Determining in advance the mixture of goods that maximizes the utility and then purchasing this mix. (2) The procedure of trial and error. (3) Making marginal decisions ti

In an uncertain globe, people are supposed to try to make best use of their satisfaction by: (1) Determining in advance the mixture of goods that maximizes the utility and then purchasing this mix. (2) The procedure of trial and error. (3) Making marginal decisions ti

18,76,764

1929670 Asked

3,689

Active Tutors

1455696

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!