Average variable costs per generic of pure competitor

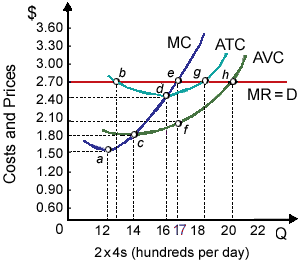

Average variable costs per generic 2×4 of this pure competitor’s equal roughly: (w) $0.20 (20¢ per 2×4). (x) $1.00 per 2×4. (y) $1.70 per 2×4. (z) $2.10 per 2×4. Can someone explain/help me with best solution about problem of Economics...

Average variable costs per generic 2×4 of this pure competitor’s equal roughly: (w) $0.20 (20¢ per 2×4). (x) $1.00 per 2×4. (y) $1.70 per 2×4. (z) $2.10 per 2×4.

Can someone explain/help me with best solution about problem of Economics...

The arbitrager is an organization or individual that will: (1) Simultaneously purchase low and sell high in various markets. (2) Create disparities among prices in various markets. (3) Resolve disputes among sellers and consumers. (4) Purchase low and

A demand curve which is perfectly price elastic is demonstrated into: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Q : Drop in interest rates of capital market Any drop in interest rates caused through people’s increased willingness to save, which will cause: (w) the rate of return schedule reflected in I0 to shift to the right. (x) the rate of return schedule reflected within I0 to shift to the left.

Any drop in interest rates caused through people’s increased willingness to save, which will cause: (w) the rate of return schedule reflected in I0 to shift to the right. (x) the rate of return schedule reflected within I0 to shift to the left.

Can someone help me in finding out the right answer from the given options. One of the advantages of a partnership over proprietorship is: (i) In a partnership just one partner is liable for the debt. (ii) Partnerships permit for more specialization in the management.

Purely competitive buyers and sellers are: (w) price-takers. (x) price-makers. (y) powerless to make decisions. (z) quantity-takers. Hello guys I want your advice. Please recommend some views for above Econ

Elucidate the role of margin requirements for correcting deflationary gap.

A profit-maximizing monopolistically competitive firm will operate where is: (w) MR > MC. (x) MR = MC. (y) P < MR. (z) P < MC. Can anybody suggest me the proper explanation for given problem regarding

Can someone please help me in finding out the precise answer from the following question. The firm’s total revenue minus its net economic costs equivalents its: (1) Economic profit. (2) Taxable income. (3) Marginal income. (4) Accounting profit. (5) Psychic inco

A purely competitive firm adjusts production therefore its marginal costs equivalent the market price, thus: (w) minimizing losses or maximizing profit. (x) ensuring that total costs do not exceed total revenue. (y) surviving the shor

A company consists $27 per unit in variable costs and $1,000,000 annually in fixed costs. Demand is predicted to be 100,000 units annually. Determine the price if a markup of 40% on total cost is used to determine the price?

18,76,764

1941052 Asked

3,689

Active Tutors

1442279

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!