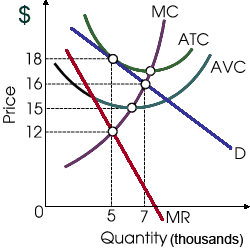

Both average variable costs and average total costs are demonstrated for this profit-maximizing firm, therefore this given figure depicts information for: (i) an oligopoly firm. (ii) operations in the short run since fixed costs are present, although we can also infer which this firm is in long run equilibrium since this is generating zero economic profits. (iii) a monopolistic competitor. (iv) a pure competitor in the output market along with some market power while buying resources. (v) a pure monopoly.

How can I solve my Economics problem? Please suggest me the correct answer.