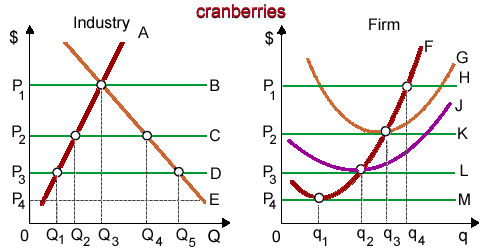

Can someone specify correct answer of the given query of demonstrated figure in below that curve J is that cranberry of: (w) industry’s supply curve. (x) firm’s demand curve. (y) firm’s average variable cost curve. (z) firm’s short-run supply curve.

Please choose the right answer for the same..