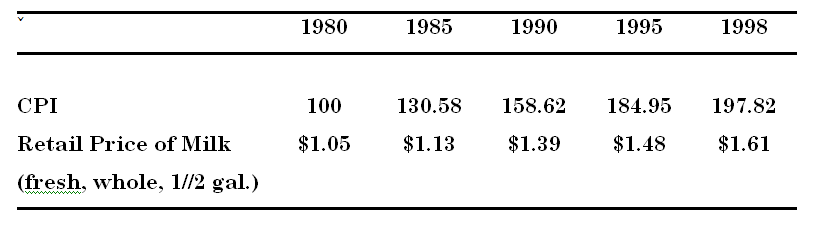

Answer the question based on given table of average retail price of milk and the Consumer Price Index from the year 1980 to 1998.

Determine percentage change in the real price (1990 dollars) from the year 1990 to 1995? Compare this with your answer in (b). What do you notice? Describe.

Percentage change in real price from the year 1990 to 1995 =1.26-1.39/1.39 . This answer is approximately identical (except for rounding error) to the answer attain for part b. It does not matter which year is selected as the base year.