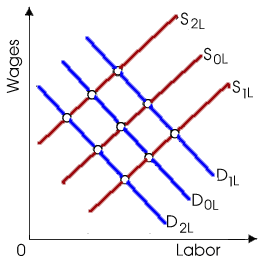

When this purely competitive labor market is primarily in equilibrium at D0L, S0L and after that excessive job safety standards are imposed through law, a new equilibrium will be attained at: (1) D0L, S0L. (2) D2L, S2L. (3) D2L, S0L. (4) D1L, S1L. (5) D1L, S2L.

How can I solve my Economics problem? Please suggest me the correct answer.