Arsing short-run shut-down point in firm

The Christmas tree farm’s short-run shut-down point arises at a price of: (i) P1. (ii) P2. (iii) P3. (iv) P4. (v) Not computable from these figures. Can anybody suggest me the proper explanation for given problem regarding Economics generally?

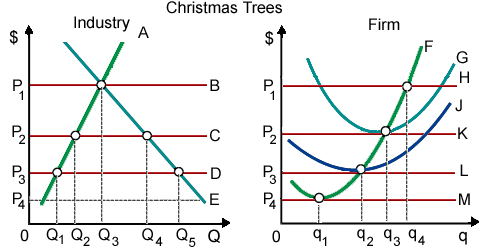

The Christmas tree farm’s short-run shut-down point arises at a price of: (i) P1. (ii) P2. (iii) P3. (iv) P4. (v) Not computable from these figures.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?

Pure competitors in a long-run equilibrium are paid a price which: (i) allows recovery of any previous operating losses. (ii) equals MC although exceeds average cost. (iii) maximizes average revenue minus average cost. (iv) equals maximum long run ave

Can someone please help me in finding out the accurate answer from the following question. Needs for all the workers to pay union dues or the equivalent are features of collective bargaining agreements that firms will function: (1) An open shop. (2) A closed shop. (3)

Every point beside a vertical demand curve (when there was such a thing) would include a price elasticity coefficient equivalent to: (1) 1. (2) 1. (3) zero. (4) infinity. (5) 1/2. Hey friends please giv

Price elasticity of demand for a good will tend to rise as the: (i) Number of reasonably good replacements available rises. (ii) Consumer income level rises. (iii) Good is a less significant budget item. (iv) Time permitted for response reduces. (v) Elasticity of supp

Since of the high probability of bankruptcy and default of a latest corporation, new corporations: (i) Encompass little trouble selling bonds. (ii) Would prefer to the issue stock. (iii) Encompass more trouble selling bonds than the established corporations. (iv) Woul

The union strategy which prevents the non-union employees of the firm from being free riders is to negotiate a contract which needs the firm to be a/an: (i) Agency shop. (ii) Open shop. (iii) Collective bargaining shop. (iv) Closed shop. (v) Union shop.

Illustrations of homogeneous goods would not comprise: (i) wheat. (ii) athletic shoes. (iii) penicillin. (iv) generic bleach. (v) reams of generic printer paper. I need a good answer on the topic of Economi

Fiscal deficit: When TE (RE + CE) > TR (RR + CR) of the government, excluding borrowing. It is termed as fiscal deficit.

Pure competition yields economic efficiency through: (w) punishing profit maximizing behavior. (x) forcing firms to adopt the least costly technologies available. (y) generating high profits as incentives. (z) rewarding entrepreneurs

When all US Treasury bonds are perpetuities that annually pay the sum of one thousand and 00/100 dollars [$1000] per annum, always, to the holder of this bond starting one year from today, at an interest rate of 4 percent, the price of this bond is: (

18,76,764

1924257 Asked

3,689

Active Tutors

1424744

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!