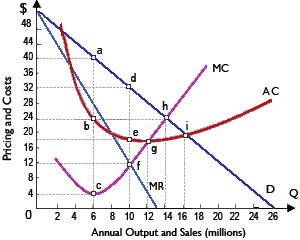

St. Valentine’s Day software is currently going addicted to version 6.0. The level of output consequent to the point where demand has unitary price elasticity is approximately: (i) 4 million copies. (ii) 6 million copies. (iii) 9 million copies. (iv) 11 million copies. (v) 13 million copies.

Hello guys I want your advice. Please recommend some views for above Economics problems.