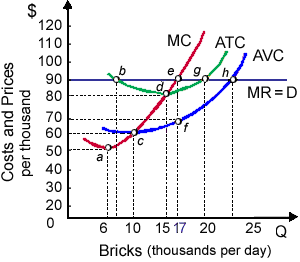

Approximate total revenue for profit-maximizing

For this profit-maximizing brickyard the total revenue equals approximately: (i) $600 per day. (ii) $900 per day. (iii) $1200 per day. (iv) $1530 per day. Hello guys I want your advice. Please recommend some views for above Economics problems.

For this profit-maximizing brickyard the total revenue equals approximately: (i) $600 per day. (ii) $900 per day. (iii) $1200 per day. (iv) $1530 per day.

Hello guys I want your advice. Please recommend some views for above Economics problems.

Lauren launched Staplex developed in Staplex, Iowa 10 years ago. The Staplex has expanded and now produces similar staplers in all ten of its factories extend across three continents. Staplex is the: (1) Horizontally integrated firm. (2) Monopoly cartel. (3) Diagonall

When the resource market demonstrated in this figure is into equilibrium: (1) owners of these resources currently receive no economic rents. (2) economic rent is specified from trapezoid Oade. (3) the rectangle Obde measures consumer surplus by the fi

A price ceiling set below equilibrium will raise the: (w) quantity supplied. (x) good’s opportunity cost to buyers. (y) sellers’ profits. (z) rate of excess supply. How can I solve my economics

Increasing equality within the distribution of income or wealth is generally related with: (1) decreases in the population’s total amount of income or wealth. (2) lower values for the Gini coefficient. (3) greater overall curvat

“Welfare by the poor to the rich” is best illustrated when: (1) an l8 year old dishwasher pays Social Security taxes to give payments to a 67 year old retired vice president of General Motors. (2) federal highway funds are diverted to a ma

Total cost for that monopolistic competitor in shown below figure equals area: (w) 0cbQ. (x) 0deQ + dcbe. (y) 0paQ cpab. (z) All of the above. Q : Circular flow of Income Elucidate the Elucidate the circular flow of Income in two sector model. Answer: There are just two sectors namely: Firms and households. Households give factor services to the fi

Elucidate the circular flow of Income in two sector model. Answer: There are just two sectors namely: Firms and households. Households give factor services to the fi

This monopolistic competitor generates Q0 output where is: (1) MR = MC. (2) MSB > MSC. (3) average cost is not minimized. (4) P = ATC. (5) All of the above. Q : Maximized output level and zero When all production costs for a monopoly are fixed [MC =0], in that case economic profit: (i) falls when price is raised in the inelastic range of a demand curve. (ii) rises when price is cut in the inelastic range of

When all production costs for a monopoly are fixed [MC =0], in that case economic profit: (i) falls when price is raised in the inelastic range of a demand curve. (ii) rises when price is cut in the inelastic range of

Supposing that the competitive firms should seek the maximum profits to survive signifies that: (1) Firm do not make trial-and-error decisions. (2) Each and every firm always seeks the maximum gain and nothing else. (3) Competition is very profitable.

18,76,764

1947416 Asked

3,689

Active Tutors

1423437

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!