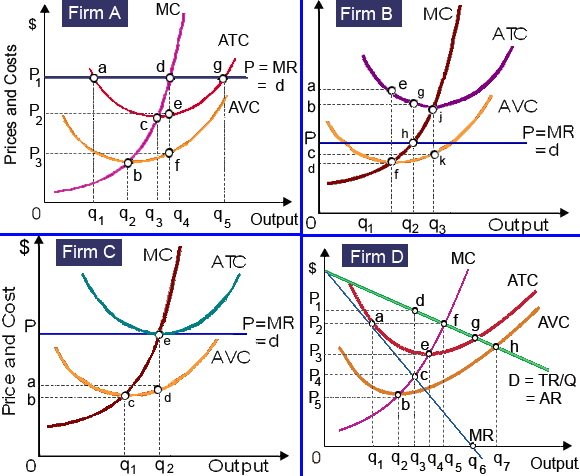

In this figure the firm probably to go out of business the soonest would be as: (w) Firm A. (x) Firm B. (y) Firm C. (z) Firm D.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.