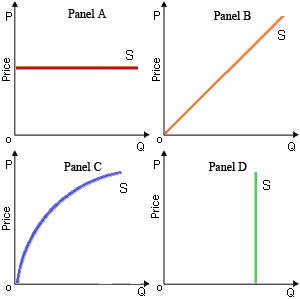

The amount of output supplied is exactly proportional to the price therefore the price elasticity of supply equivalents one into: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D.

Please choose the right answer from above...I want your suggestion for the same.