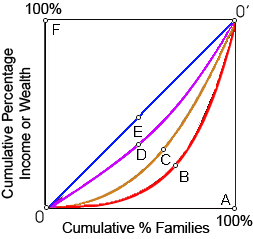

Absolute and complete inequality into the distribution of income or wealth would be reflected within the Lorenz curve demonstrated as: (i) line 0A0'. (ii) line 0B0'. (iii) line 0C0'. (iv) line 0D0'. (v) line 0F0'.

Hey friends please give your opinion for the problem of Economics that is given above.